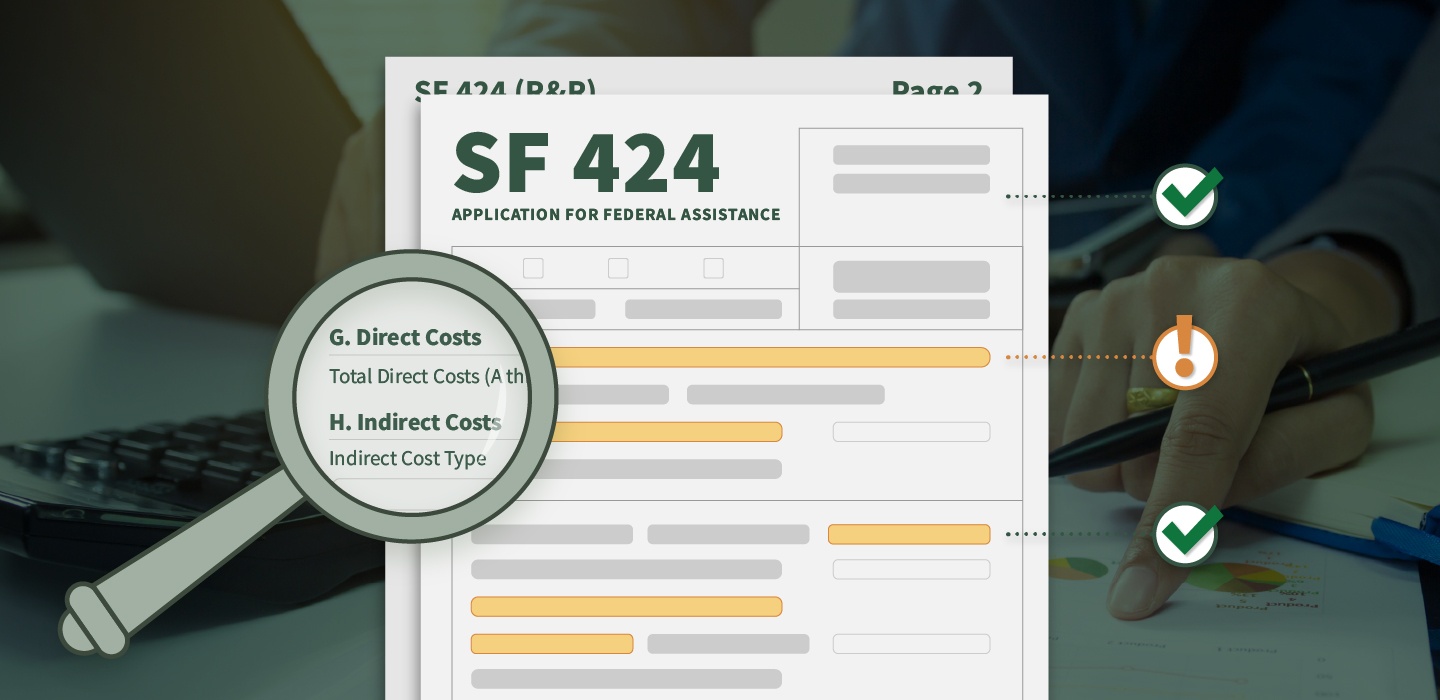

Government contracts and grants demand FAR-compliant accounting. This white paper will give you all the basic information you need to navigate the rules and regulations, set up a compliant accounting system, and avoid trouble.

You have a federal grant that requires a Uniform Guidance Audit. In the second blog in our series, we walk you through every step of the UGA so you know what to expect and how to avoid trouble.

You may have heard about the Uniform Guidance Audit, but does your government grant require one? The first blog in our 7-part UGA series starts at the beginning and gives you all the information you need.

Staying FAR-compliant is pivotal to your government award. This in-depth guide details what needs to be done and by whom, while providing actionable steps and explanations.