NEXT WEBINAR • 11/04/2025

"Understanding the Strings to Your Federal Funding Vehicle"

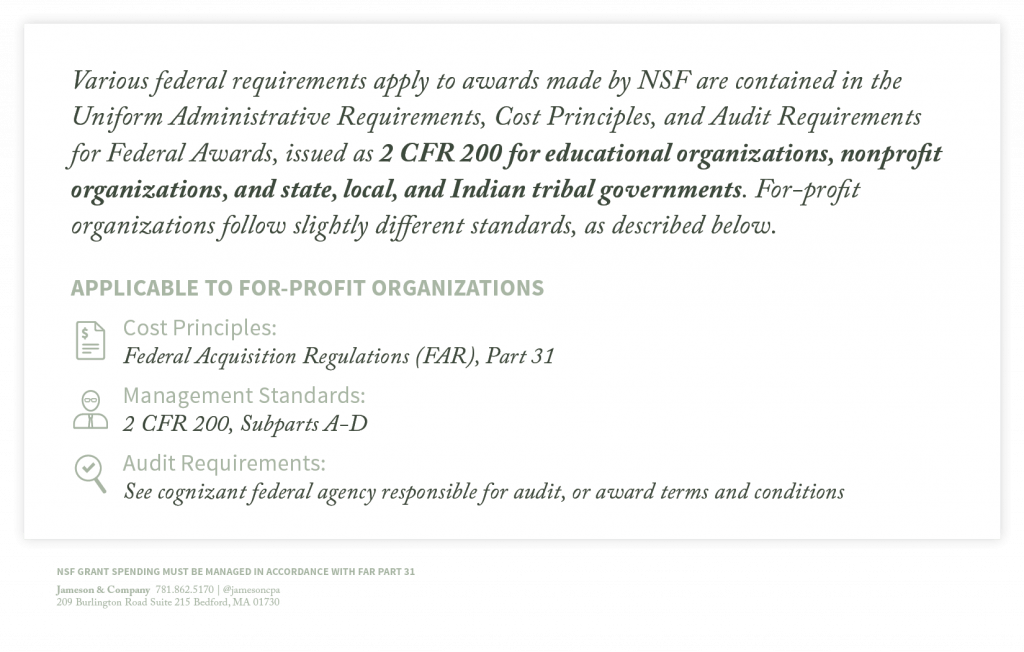

REGISTER HEREIf you’re a for-profit business with an NSF grant, you must comply with the Proposal & Award Policies and Procedures Guide (PAPPG), which requires Federal Acquisition Regulation (FAR) Part 31 accounting.

The National Science Foundation was created by Congress in 1950 to promote the progress of science. Today, the agency uses an annual budget of $8.3 billion (FY 2020) to initiate and support scientific and engineering research, issuing approximately 12,000 grants a year for an average duration of three years.

The vast majority of NSF grant funding goes to colleges, universities, and hospitals, so the rules and regulation that stem from 2 CFR 200 are written for non-profits. To make it clear that these regulations also apply to for-profit awardees, the NSF tried to provide clarity by issuing the paragraph below.

With other agencies, an audit gives the awardee the chance to make things right if there was a mistake. The lack of audit oversight can create a false sense of security.

When your grant is over, you must prepare a Final Spending Report. Any funding not spent “properly” must be repaid based on the agency’s analysis of this report.

With other agencies, an audit gives the awardee the chance to make things right. With NSF grants, problems in the Final Spending Report can trigger an immediate investigation by the Inspector General (IG)* and fast track to criminal prosecution under the False Claims Act.

For more details, read our blog on this subject.

Obviously, your best course of action is to avoid trouble by staying compliant. To help, we’ve created a comprehensive solution for for-profit NSF grantees which includes:

Fill out the form and one of our government funding experts will be contacting you within 48 hours.